FINCEN Real Estate Reporting Rule Is Now in Effect: What San Francisco Buyers Using LLCs or Trusts Should Know

Not long ago, I was standing in the entry of a Pacific Heights home while a buyer studied the ceiling moldings and the proportions of the living room. The conversation drifted, as it often does in San Francisco, from architecture to renovation costs and then to something less visible but just as important. How the property should be held.

Around here, that question rarely has a simple answer. Sometimes it is an LLC created for liability protection. Sometimes it is a family trust that has quietly held property for years. Occasionally, it is a layered structure built by an attorney and an accountant who both have strong opinions about how ownership should work.

Those structures are normal in The City. What is new is the federal reporting rule that now sits quietly behind them.

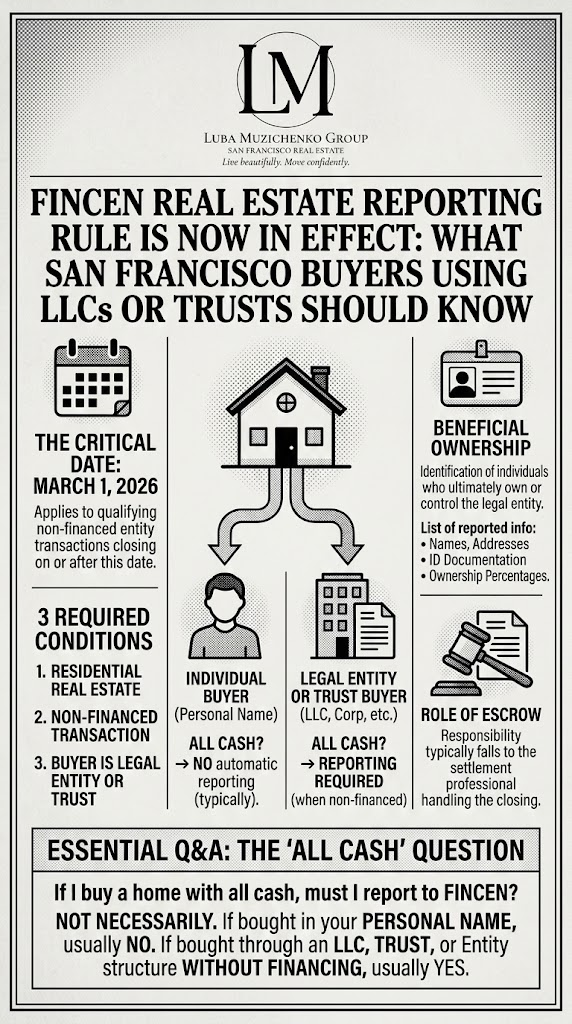

As of March 1, 2026, the U.S. Treasury’s Financial Crimes Enforcement Network, better known as FINCEN, began enforcing a nationwide rule that requires reporting on certain non-financed residential real estate purchases when the buyer is a legal entity or certain trust structures.

I will admit something up front. I meant to write about this earlier. The rule was finalized, then delayed, and for a while it felt like something that lived mostly in compliance bulletins and legal briefings. Now that it is active, it has moved from theory into the background mechanics of real transactions.

The rule applies based on the closing date. If a qualifying transaction closes on or after March 1, 2026, the reporting requirement now applies.

So what actually triggers reporting?

In most cases three conditions need to exist at the same time. The property must be residential real estate, the transaction cannot involve an institutional lender, and the buyer must be a legal entity or certain trusts rather than an individual.

That includes LLCs, corporations, partnerships, and some trust structures that acquire property without financing.

What often surprises people is what does not automatically trigger the rule.

Paying cash alone is not enough. If someone buys a home in their personal name without a lender involved, the rule usually does not apply. The moment that same purchase happens through an LLC or certain trusts without financing, reporting generally does apply.

Clients often ask a very practical question once they hear about this rule, and it usually comes up in the middle of a conversation about how to hold title. If someone buys a home in San Francisco all cash, do they now have to report the purchase to FINCEN?

The answer depends entirely on how the property is held. A purchase in an individual’s personal name typically does not trigger the rule. A purchase through an LLC, partnership, corporation, or certain trusts without financing usually does.

The buyer does not normally file the report themselves. In most transactions the responsibility falls to the settlement professional handling the closing. In San Francisco that typically means the escrow company.

Escrow, however, cannot file the report without information from the buyer.

The filing focuses on beneficial ownership. In simple terms, the individuals who ultimately own or control the entity acquiring the property must be identified, along with ownership percentages and basic identifying documentation.

This information does not appear publicly the way a recorded deed does, and it will not show up in the MLS. What changes is that entity-based purchases are no longer anonymous at the federal level.

In practical terms the impact in San Francisco will show up mostly in preparation.

Transactions here rarely move in straight lines. Buyers are coordinating contingent sales, trust distributions, renovation planning, and family ownership structures at the same time. When the entity documents are organized and ownership is clear, escrow moves smoothly toward closing.

When those documents live in three different offices and have not been revisited in years, the process slows down exactly when buyers want certainty.

Because FINCEN requires the report to be filed within thirty days of closing, escrow professionals will want clarity about beneficial ownership during the closing process rather than after the fact.

Who will notice the rule most in The City?

Buyers purchasing through LLCs, investors using entity structures, trust ownership that falls within the rule, foreign nationals acquiring property without financing, and family offices that traditionally hold real estate through entities.

Buyers obtaining conventional financing in their personal names will rarely feel any difference because lenders already operate under similar anti-money-laundering reporting frameworks.

San Francisco real estate has always existed inside layers of regulation. Historic preservation, seismic upgrades, planning review, and condo conversion rules are simply part of the environment here. The FINCEN rule becomes another quiet layer that sits behind the transaction.

The homes themselves often reflect decades of careful design decisions. The ownership structures beneath them tend to follow the same philosophy.

If you are planning to purchase property through an LLC or trust now that the rule is active, it is worth reviewing the ownership structure before you start writing offers. Most of the time nothing about the structure itself needs to change. What matters is that the documentation behind it is clear, organized, and ready for escrow.

A quick conversation early can prevent delays later, especially in a competitive San Francisco transaction where timing matters. If you want to walk through your structure and make sure everything is in order before moving forward, reach out and we can take a look together.